What is a Payment Service Provider (PSP) and How Do They Work?

Published on May 15, 2025

• By Volkan Arisli

Introduction: The Backbone of Online Transactions

In today's digital economy, seamless online transactions are not just a convenience but a necessity. Businesses of all sizes rely on efficient payment processing, yet often grapple with the complexities of integrating and managing multiple payment systems. But what exactly happens behind the scenes when a customer clicks "Pay Now," and how can this process be streamlined? This is where Payment Service Providers (PSPs) come into play, acting as crucial intermediaries that make online commerce possible and manageable.

This article will demystify PSPs, explaining what they are, their core functions, how they work, and why understanding them is vital for any business aiming for operational efficiency and financial clarity online.

What is a Payment Service Provider (PSP)?

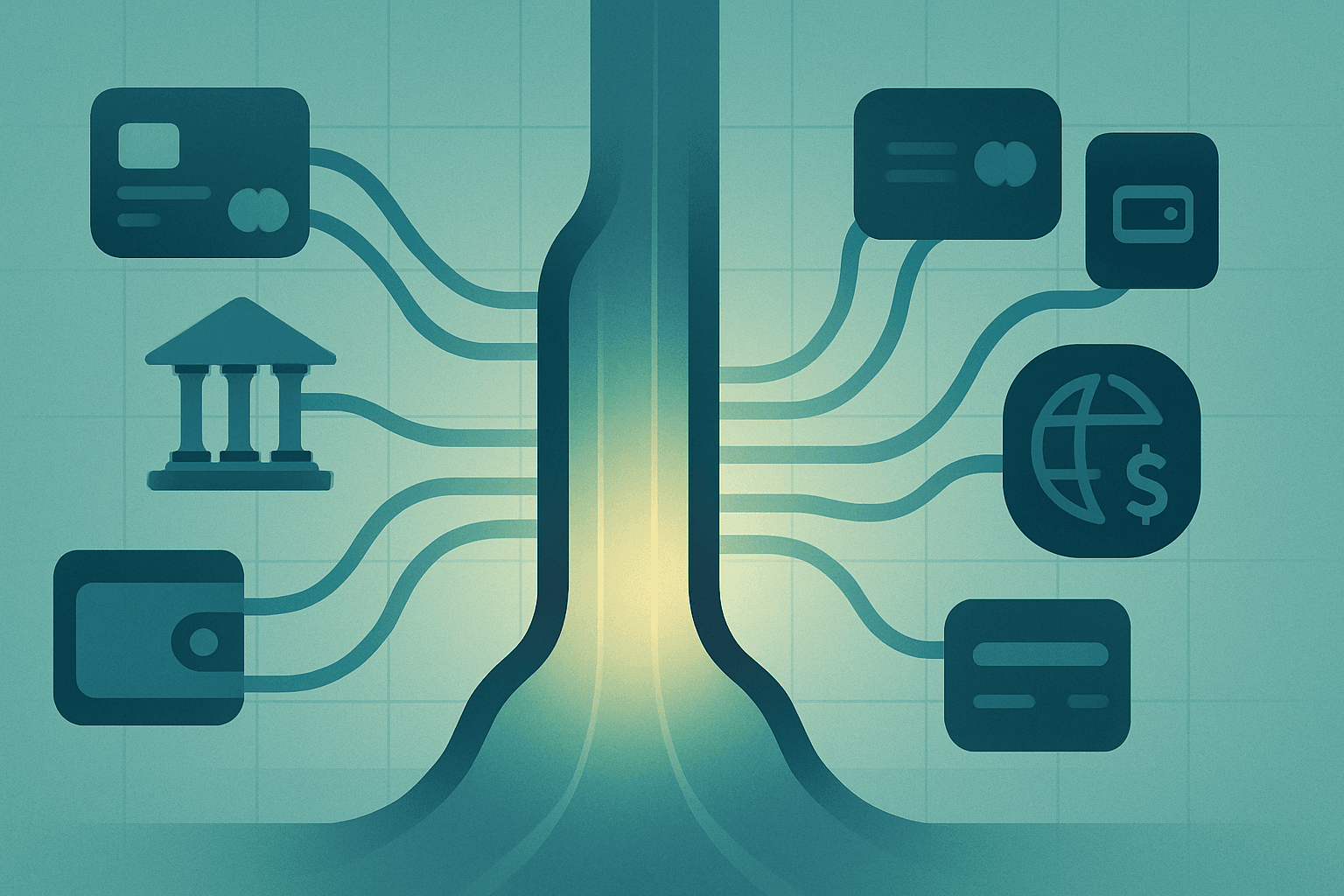

A Payment Service Provider (PSP) is a third-party company that enables businesses (merchants) to accept a wide range of electronic payment methods. These can include credit cards, debit cards, bank transfers (like ACH or SEPA), e-wallets (like PayPal or Apple Pay), buy now pay later (BNPL) services, and more.

Essentially, a PSP connects a merchant's website or application to the broader financial network, including acquiring banks, card networks (Visa, Mastercard, American Express), and other payment systems. They offer a single integration point to access multiple payment methods, significantly simplifying what would otherwise be a fragmented and resource-intensive setup for individual merchants, prone to data silos and reconciliation headaches.

Key Takeaway: PSPs are financial service companies that offer merchants a unified solution for accepting electronic payments through various methods, simplifying integration and enhancing security.

Core Functions of a PSP

PSPs perform several critical functions to facilitate smooth, secure, and manageable transactions:

- Payment Processing: This is the primary role. PSPs efficiently route transaction data between the merchant, the customer's bank (issuing bank), and the merchant's bank (acquiring bank), ensuring funds move correctly.

- Merchant Account Provision: Many PSPs offer or facilitate merchant accounts, a specialized bank account necessary for businesses to accept card payments, streamlining another setup step.

- Payment Gateway Services: They provide the secure technology (the payment gateway) that captures and transmits payment information, acting as a protected bridge between the merchant's platform and the payment processor.

- Security and Fraud Prevention: PSPs invest heavily in robust security measures, including PCI DSS compliance, tokenization, encryption, and advanced fraud detection tools. This significantly reduces the security burden and risk for merchants.

- Multi-Currency Processing: For businesses selling internationally, PSPs capably support transactions in multiple currencies and handle conversions, simplifying global sales and financial reconciliation across markets.

- Reporting and Analytics: PSPs typically provide dashboards and downloadable reports that give merchants vital insights into transaction history, sales trends, and fee structures. This data is crucial for financial analysis, easier reconciliation, and potentially identifying revenue leakage or cost-saving opportunities.

- Integration with Shopping Carts & Platforms: They offer seamless integrations (plugins, APIs) with popular e-commerce platforms (Shopify, WooCommerce, etc.) and business systems, reducing development time and ensuring data flows smoothly.

How Does a PSP Work? The Transaction Flow

While the customer experiences a quick, seamless payment, a complex and highly secured series of steps occurs in seconds:

- Customer Initiates Payment: The customer selects items and proceeds to checkout, choosing their preferred payment method on the merchant's site.

- Secure Data Transmission: The PSP's payment gateway securely captures and encrypts the customer's payment details (e.g., card number, expiry date, CVV).

- Routing to PSP: The encrypted information is securely transmitted to the PSP.

- Transaction Authentication & Fraud Checks: The PSP, often in conjunction with its partners, performs initial fraud checks and authenticates the transaction (e.g., using 3D Secure for cards) to minimize risk.

- Routing to Card Network/Bank: For card payments, the PSP routes the transaction to the relevant card network (Visa, Mastercard, etc.), which then forwards it to the customer's issuing bank.

- Authorization by Issuing Bank: The issuing bank verifies funds/credit and card validity, then approves or declines the transaction.

- Response to Merchant: The approval or decline message travels back securely through the card network to the PSP, then to the merchant's website, informing the customer and triggering order fulfillment processes if successful.

- Settlement: If approved, the funds are eventually transferred from the issuing bank to the acquiring bank (merchant's bank). The PSP facilitates the consolidation and deposit of these funds into the merchant's account, net of fees, according to an agreed schedule. This managed settlement process simplifies cash flow forecasting for the merchant.

Important Note: The exact flow can vary based on the payment method and PSP, but the emphasis on security and reliability remains constant.

Benefits of Using a PSP

For businesses, particularly finance and operations leaders, partnering with a PSP offers numerous strategic advantages:

- Simplicity & Reduced Complexity: A single integration provides access to multiple payment methods and currencies, drastically reducing IT overhead and vendor management.

- Enhanced Security & Compliance: PSPs handle sensitive data and compliance requirements (like PCI DSS), reducing the merchant's direct risk and liability.

- Cost-Effectiveness: Often more affordable due to aggregated transaction volumes and reduced need for in-house security infrastructure or multiple direct integrations.

- Faster Market Entry & Scalability: Quicker to implement online payments and easier to scale operations globally or add new payment methods.

- Global Reach, Localized Experience: Easily accept payments from international customers in their preferred currencies and methods.

- Improved Conversion Rates: Offering a variety of familiar and trusted payment options can reduce cart abandonment and build customer trust.

- Centralized Data & Valuable Insights: Access to consolidated transaction data, fraud management tools, analytics, and often recurring billing features, leading to better financial oversight.

Conclusion: Strategic Enablers of Modern Commerce

Payment Service Providers are vital components of the digital commerce ecosystem. They do more than just process payments; they simplify the inherent complexities of online transactions, bolster security, and empower businesses to serve a global customer base with diverse payment preferences. By offering a unified and efficient platform for managing transactions, PSPs allow merchants to focus on their core business objectives, armed with greater financial clarity and operational control.

Choosing the right PSP is a significant strategic decision for any online business, directly impacting operational efficiency, risk management, customer experience, and ultimately, financial performance and profitability.

Get Expert Insights on Payment Finance

Subscribe to our newsletter for deep dives into payment optimization, cost reduction strategies, and financial data analytics.